NFT doom — off-chain execution of on-chain agreements.

Krishang Nadgauda / May 20, 2021

6 min read

Introducing off chain entities to the on-chain world is a classic challenge in crypto.

An explicit instance of this challenge is framed as the 'oracle problem' — the problem of introducing reliable and honest, real world data onto our on-chain, distributed database. Oracles are often associated with price feeds (e.g. how much Ether or an ERC 20 token costs in an off chain denomination like USD) or with information that people bet on in on-chain prediction markets.

In the case of these oracles, what we witness is, in some sense, 'on chain executions informed by off chain data'. The off chain data introduced by oracles plays a role in determining what smart contract code will be executed upon its introduction on chain. Take, for example, the Augur prediction market for the 2020 US presidential election results. A participant in this prediction market participates by locking their bet money into a smart contract. Whether that participant loses the locked money, or has the money plus winnings sent to their ethereum account is determined by off chain data — the relevant fact about the election results in question.

It's simple to see why the integrity of off chain data is critical. You can't revert on-chain transactions whether or not it was dishonest off chain data that informed the transaction. In this way, when it comes to oracles like price feeds or the ones propping up prediction markets, we witness 'on chain executions informed by off chain data'.

In some sense, the whole idea of introducing off chain data to the on-chain world feels contra to the on-chain ethos. However, decentralized oracles that maintain some level of that on-chain ethos have popped up over time. And so, the vulnerability of having to trust that the relevant off chain data is honest, is not so critical. The crypto ecosystem has managed to pull off on chain executions informed by off chain data without abandoning, at least wholly, the on-chain ethos.

All of that said, there's another kind of off chain data on the horizon whose trust requirements are somewhat uncomfortable. I'm talking about NFTs.

NFTs, in a way, turn the oracle model of 'on chain executions informed by off chain data' upside down. What we witnessed throughout the NFT craze of early '21 is 'off chain executions of on chain agreements'. This is a phenomenon that, I argue, will only continue to grow more significant, and make everyone's inner crypto soul — the one yearning for true decentralization — feel uncomfortable.

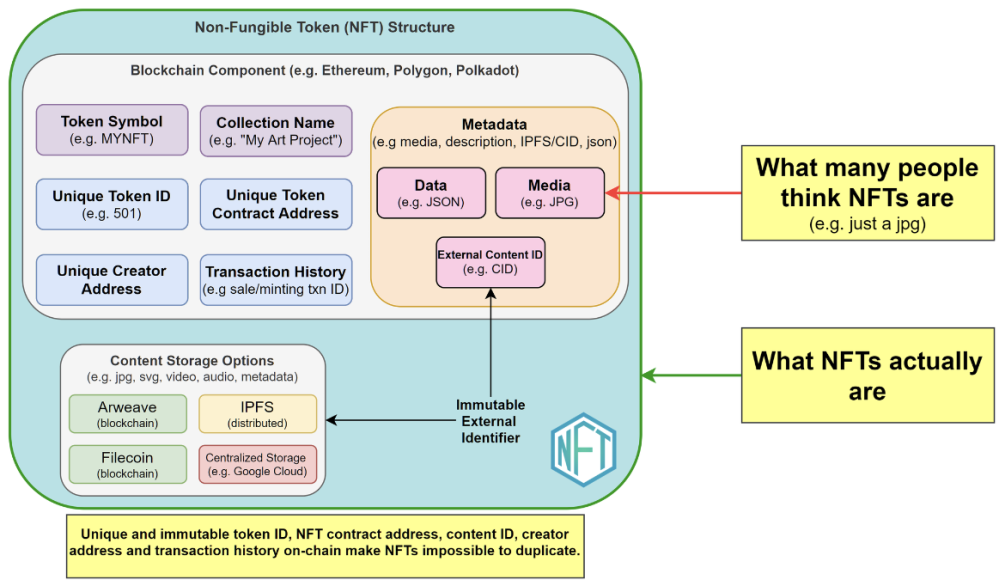

NFTs are perhaps one of the most general concepts to have emerged in crypto. Let's forget the "Non fungible" part for a minute — that's not the most exciting part about NFTs, regardless of all the press it gets. One of the core, and most exciting features of an NFT is, simply, that it "tokenizes" something. On chain, an NFT represents an off chain object. An NFT represents an off chain object in the form of an agreement. When you buy an NFT, what you buy is a certain claim on the off chain object it represents. Generally, this claim is a claim of ownership.

Let's consider an example. Beeple sold an NFT for $69 million USD to Metakovan. The NFT in question is not just the artwork, which is, in some sense, the display picture of the NFT. The NFT is an agreement that the person recognized as the owner of the NFT (Metakovan) by the creator of the NFT (Beeple), shall have a claim of ownership on the NFT's relevant off chain object (the artwork jpeg).

Note: I won't go so far as to start defining "ownership" and so on — we'll accept these things as primitives for this post.

Tokenizing things like artworks as an NFT is, as you might've expected me to say next, just the beginning. It is likely a matter of time that, like artwork, things from concert tickets to property rights get tokenized as NFTs. This is where things get interesting and even more uncomfortable than the multi million dollar NFT doomer headlines.

With the introduction of tokenized concert tickets, property rights and so on, we'll witness, in its explicit form, people honoring on chain agreements, off chain. What's key, here, is that the place of execution is off chain, unlike with oracles, where the place of execution is on chain.

This makes a world of difference. When the place of execution is on chain, the execution is trustless to the extent that the off chain data it depends on is honest. Thanks to the existence of decentralized oracles like Chainlink, we may deem this to be acceptable, in the context of the on-chain ethos. However, when the place of execution is off chain, it's a different story.

There's a reason we have overcollateralized loans in the DeFi ecosystem. This is somewhat of an on-chain law — any piece of an on-chain process that requires trusting the off chain execution of something, usually has a punishable counterpart on chain. NFTs, even right this moment, break this law. A concert ticket NFT means nothing (except possibly the 'exclusivity' of the ticket) if there is no concert. Certainly, a tokenized legal agreement means nothing if it isn't legally enforceable off chain. In the case of artworks, you better hope the artist hasn't tokenized the artwork on a duplicate contract, making it unclear which one's cannon.

Make of this what you will. Maybe this means that what the NFT ecosystem needs the most isn't pixelated humans and dogs, but legal clarity or restructuring. Perhaps the host of uncomfortable motifs around NFTs result in a new NFT EIP. Regardless of how it plays out, and whether or not we ever see another $69 million dollar NFT sale, the core concept of tokenizing off chain objects is here to stay. We better start converging on a way to handle this, or converge on the idea that we're all okay with not converging on a standard for handling it all.

The week of the crash is a nice time to have discussions like these. As the sage Andre Cronje says — Bull run, bear development. Bear run, bull development.